Relevant Cost & Short term decisions

Relevant Cost ~ "Costs which are affected by the decision being taken"

In other words ‘the amount by which costs increase and benefits

decrease as a direct result of a specific management decision"

Before the management of an enterprise can make

an informed decision on any matter, they need to incorporate all of the

relevant costs which apply to the specific decision at hand in their decision

making process.

Identifying relevant and non-relevant costs

The identification of relevant and non-relevant

costs in various decision-making situations is based primarily on common sense

and the knowledge of the decision maker of the area in which the decision is

being made.

Non-relevant costs

-Sunk costs

-Fixed overheads that will not change due to the decision

-Committed costs

-Depreciation

-Notional costs

-Sunk costs

-Fixed overheads that will not change due to the decision

-Committed costs

-Depreciation

-Notional costs

Are variable costs always relevant costs ? No, if the variable costs have already been incurred (sunk costs) or if the variable cost wont change due to the decision been taken (committed costs)

Are fixed costs always non-relevant ? No, if there is an incremental fixed cost due to the decision been taken then that incremental fixed cost will be relevant.

Opportunity costs ~ "value of the next best alternative sacrificed by the decision"

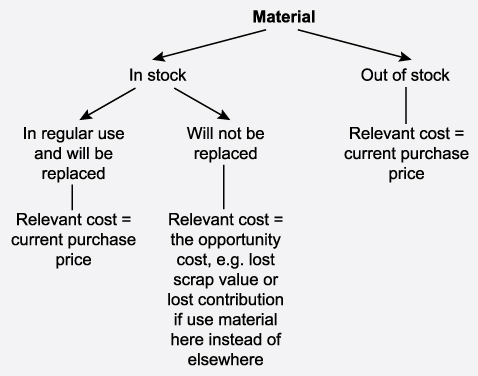

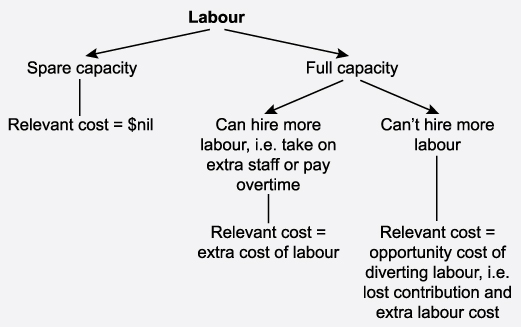

Calculating relevant cost of resources,

If available in stock & regularly used: replacement cost

If available in stock & not used: Zero

If not available in stock: purchase price

If available in stock & regularly used: replacement cost

If available in stock & not used: Zero

If not available in stock: purchase price

Minimum price quotation to special projects = Relevant cost of the project

No comments:

Post a Comment